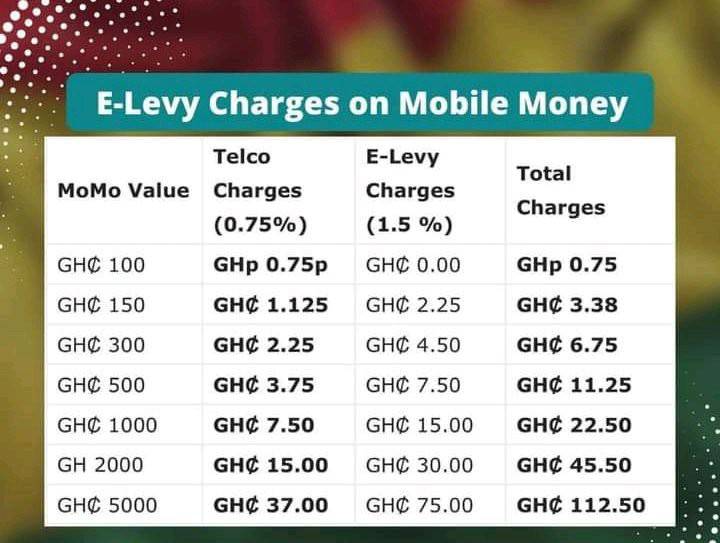

Today opened my eyes to the fact that the E-Levy actually costs more than the fees from telcos (MTN, Telecel, AirtelTigo). Currently, the levy stands at 1.50% of the total amount for electronic transfers. At first, I thought 1.50% wasn’t a big deal since it’s under 2%, so I didn’t bother to calculate it.

I usually manage my money through my bank account, using an ATM card that only charges me 5 GHS monthly, with no fees on withdrawals.

I typically transfer small amounts to my mobile number for airtime and data bundles, and occasionally send under 100 GHS to others. Because of this, I hadn’t felt the impact of the E-Levy until now.

Today, I got 500 GHS credited to my mobile wallet, bringing my total to 520 GHS. I set aside 20 GHS for airtime in case of an emergency. When I tried to buy 10 GHS of airtime, I assumed both the E-Levy and the telco would charge me 5 GHS each.

After my first attempt, I received a notification saying my balance was insufficient. Confused, I checked and saw I only had 7.5 GHS left. How could that happen? Upon reviewing my transactions, I discovered the E-Levy actually charged me 7.5 GHS, which is 2.5 GHS more than the telco fee. Overall, I ended up paying 12.5 GHS in charges.

After doing some online research, I realized that the 1.50% I had previously overlooked was actually not small. I remember advising my boss to always use mobile money for my salary since I frequently receive notifications about my bank undergoing maintenance, which can be a hassle when I need quick access to my funds.

Just think if he had taken my advice! For every 2,000 GHS, I would have faced an E-Levy of 30 GHS and telco charges of 20 GHS, totaling 50 GHS in fees. That’s outrageous!

On a brighter note, there’s a USDT wallet on Minipay through the Opera News app that lets me earn daily interest based on my balance. They charge very little for transactions, and I can access my money whenever I want.My bank, on the other hand, charges 5 GHS monthly, and I don’t earn any interest; instead, I face deductions due to fees. Plus, transferring money from my bank account to a phone number not linked to my bank incurs charges, whereas transfers to a linked number are free.

YelloSave on MTN was useful until they limited access to funds, allowing free withdrawals only once a month. Honestly, the E-Levy is a real issue because it costs more than the fees from telcos.

NB: The levy currently stands at 1.50% of the value of electronic transfers and applies to amounts over 100 GHS daily. That means the E-Levy kicks in only after cumulative transfers exceed 100 GHS in a day.

No comments yet

Be the first to share your thoughts!