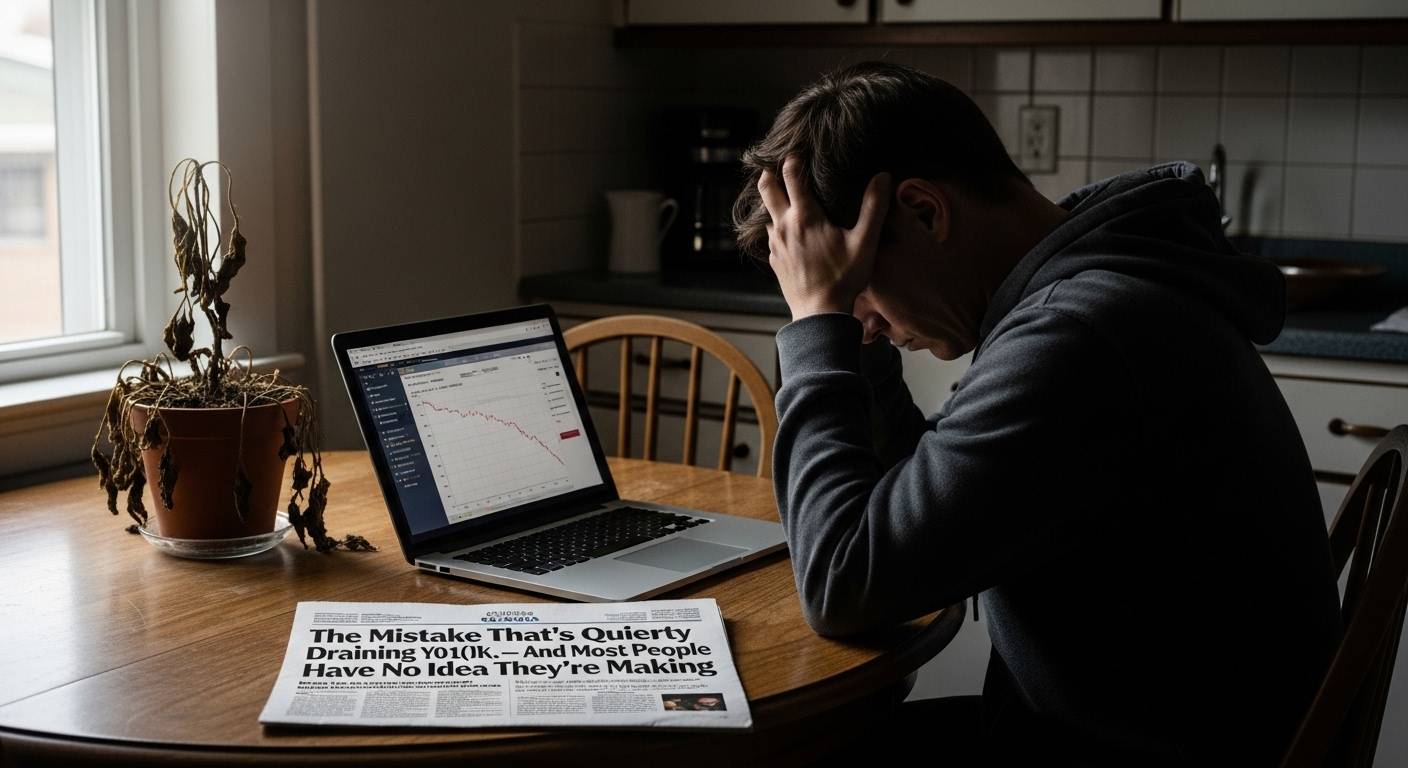

Here's something I've seen greater instances than I can be counted: a person sits down with me to review their finances, they may be doing reasonably well, after which we pull up their 401(okay). Decent stability. Regular contributions. And right there within the funding allocation screen — each dollar sitting in a cash marketplace fund, earning subsequent to not anything, even as the marketplace has been climbing for years.

They had no idea. Nobody told them. They enrolled, picked a contribution charge, and assumed the relaxation was dealt with.

It wasn't.

Most 401(ok) errors aren't created from laziness. They're comprised of silence — no one explained the policies, so people improvise.

Why This Keeps Happening

The 401(good enough) is one of the most effective financial gear maximum Americans have get entry to to. Tax-advantaged boom, potential agency contributions, compound returns over a long time — in principle, it's nearly not possible to reduce to rubble. In exercise, humans mess it up continuously.

Part of the trouble is how enrollment works. You get hired, a person from HR arms you a packet, you choose a percentage and sign something, after which existence moves on. Nobody sits you down and explains that the fund you defaulted into might be a strong price fund designed to guard towards loss — which is a pleasant way of pronouncing it slightly grows. Nobody mentions that your business enterprise might be inclined to in shape your contributions dollar for greenback as a good deal as a certain component, and that during case you are contributing beneath that threshold, you're voluntarily giving up part of your compensation.

It's now not that the records is hidden. It's just in no way made urgent.

The Mistakes That Cost the Most

After years of reviewing client financials, the mistakes I see most customarily fall into a pretty clean pattern.

Missing the company match. This one actually frustrates me due to the fact it is so fixable. If your business enterprise offers to suit your contributions as much as, say, four% of your salary, and you're contributing 2%, you're leaving cash at the table each single paycheck. It's deferred repayment you have already earned — you simply must declare it. I've run the numbers for customers who overlooked their complete healthy for ten or fifteen years. The quantities are painful to look at.

The default funding entice. A lot of human beings are contributing faithfully every month to a fund that isn't always surely invested in anything. Older plans specially generally tend to default into money market or stable price alternatives — they're secure, they do not lose value, and that they do not in particular develop either. Over thirty years, the difference among a 2% return and a 7% go back isn't a rounding mistakes. It's the difference between retiring for your phrases and working longer than you planned.

Cashing out at some point of a activity change. This one has a ripple impact human beings do not fully respect till later. When you coins out a 401(k) earlier than 59½, you pay income tax on the whole amount plus a ten% early withdrawal penalty. A $30,000 stability can internet you less than $19,000 after taxes and penalties relying in your bracket and kingdom. And the $30,000 it's long past? That's not just $30,000 misplaced — it is anything that money could have compounded into over the following twenty or thirty years. I've seen humans make this call to cover a gap among jobs and spend years regretting it.

Ignoring costs. It sounds minor. It isn't always. The distinction between a 0.05% cost ratio on an index fund and a 1.Zero% price on an actively controlled fund — interior a $three hundred,000 portfolio over twenty years — can run properly into six figures. And the actively managed fund in all likelihood might not outperform the index anyway. Check the rate ratios at the budget you maintain. Move closer to the bottom-fee alternatives your plan offers.

Why It's Worth Fixing Now

The element about retirement debts is that point does an tremendous amount of the heavy lifting — but best if your cash is sincerely running. Every yr you live within the incorrect fund, omit a fit, or carry a 401(okay) mortgage is a 12 months of compounding you do not get returned.

None of those fixes are complicated. Most of them take fifteen minutes on your plan's on line portal. Log in, check your contribution fee against your agency's fit system, study what fund your money is sitting in, and test the cost ratio. That's the whole audit.

QUICK ACTION

Log into your 401(okay) portal nowadays. Find: (1) your agency's fit formulation, (2) where your contributions are presently invested, and (three) the price ratio of every fund you keep. These three numbers will inform you the whole thing you want to understand.

The Bottom Line

A 401(k) is not a fixed-it-and-forget about-it account, despite the fact that the industry on occasion markets it that manner. It's a tool, and like any tool, it works lots better while you sincerely recognize a way to use it.

You don't need to end up a finance expert. You simply want to spend twenty mins a year paying attention. Given what's at stake, it is probably the pleasant hourly fee you may ever get.

No comments yet

Be the first to share your thoughts!